What is gamma exposure (GEX)?

+

Gamma exposure (GEX) measures how much market makers' collective delta changes for every 1% move in the underlying. High gamma at a price level means dealers must buy or sell large amounts of the underlying to stay hedged — creating predictable support, resistance, and volatility compression or expansion at that level.

Do I need to trade options to use GEX data?

+

No — and this is the edge most directional traders overlook. Market maker hedging mechanically moves the underlying: ES, NQ, SPY, QQQ, GLD, BTC, and more. Their forced buying and selling shows up on your chart as support, resistance, and momentum zones — whether you ever trade an options contract or not.

Options traders use GEX to time entries, select strikes, and manage risk around vol regimes. Directional traders use the same data to answer one question before each session: is today a range day or a trend day, and where are the structural levels that matter?

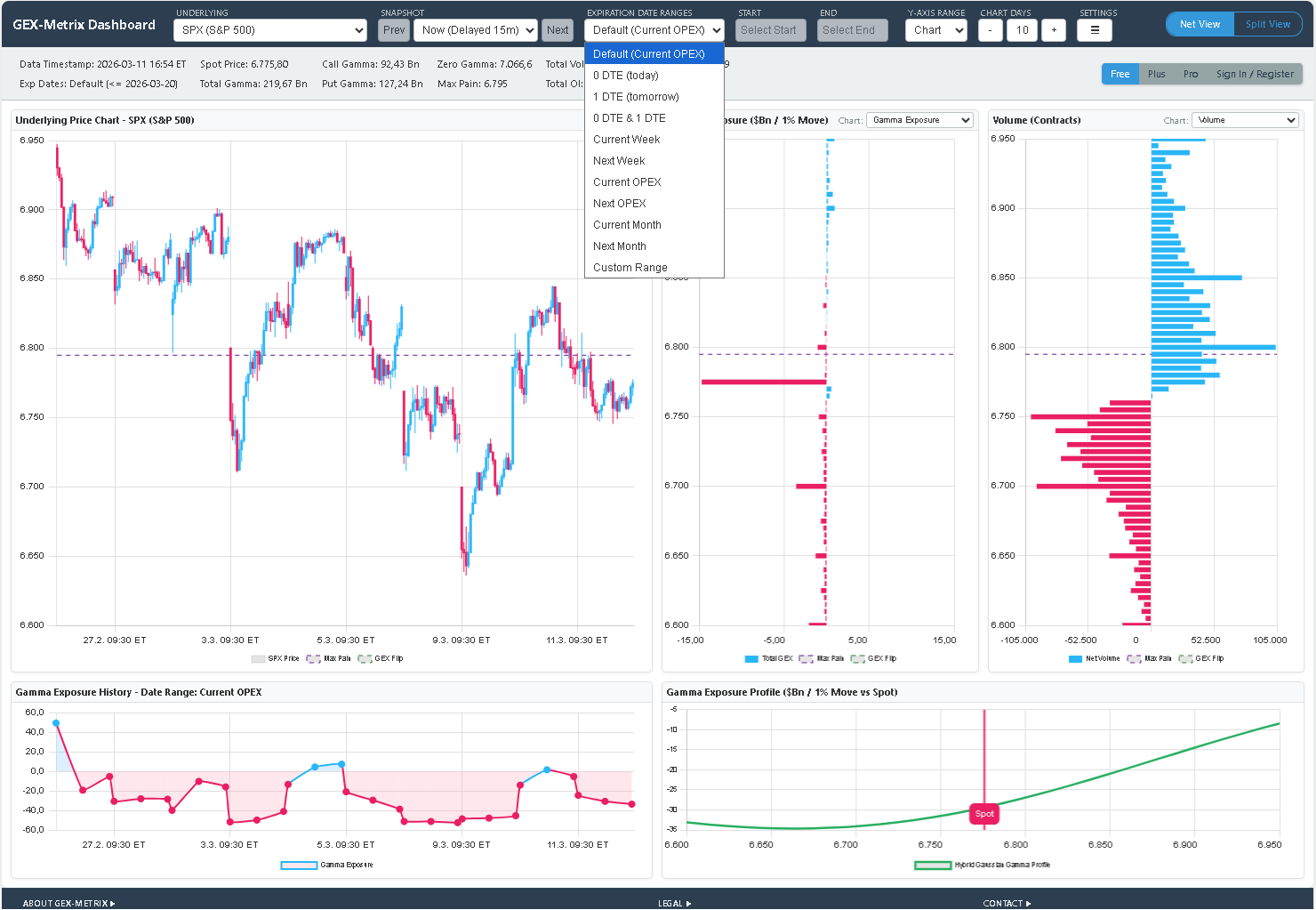

What is the zero gamma level and why does it matter?

+

The zero gamma level is where dealer gamma flips from positive to negative. Above it: dealers stabilize — buying dips, selling rallies. Below it: dealers amplify — selling declines, buying rallies. This level determines range day vs. trending day.

How do futures traders specifically use gamma levels?

+

(1) Gamma walls → fade levels in positive gamma. (2) Gamma flip → breakout trigger. (3) Negative gamma zones → momentum over mean-reversion. (4) Pre-session: positive or negative gamma sets the day's bias.

What do Gamma, Delta, Vanna, and Charm each tell me?

+

Each Greek reveals a different dimension of dealer hedging pressure:

Gamma — where dealers must hedge most aggressively as price moves. High gamma concentration at a strike creates strong support or resistance because dealer re-hedging is mechanical and large.

Delta — the directional tilt embedded in current positioning. Negative aggregate delta means dealers are structurally short the underlying, creating a headwind for rallies. Positive delta means the opposite.

Vanna — how dealer hedges shift when implied volatility changes. A VIX drop forces dealers to buy the underlying (Vanna tailwind); a VIX spike forces selling. This is the driver of "no-catalyst" rallies after volatility compression.

Charm — how dealer hedges erode as time passes. Every overnight session changes every dealer's hedge ratio. Charm flow is highest on Thursdays and Fridays, creating systematic directional pressure at the open before price moves a tick.

What is a gamma squeeze?

+

Aggressive call buying forces market makers to buy the underlying. As price rises, more OTM calls come in range — requiring even more buying. GEX data shows the buildup before it becomes obvious in price.

How often does GEX Metrix update its data?

+

Data updates every 15 minutes during market hours. Historical snapshots let you compare current positioning against prior sessions.